FDIC-Insured – Backed by the full faith and credit of the U.S. Government

FDIC-Insured – Backed by the full faith and credit of the U.S. Government

Welcome December! We’ve reached the twelfth and final month of 2025 – though it wasn’t always that way. In the original Roman calendar, December was actually the tenth month (its name comes from “decem,” meaning ten). When the calendar eventually expanded to twelve months, December held onto its name. Just as the calendar expanded and evolved, so has our industry. If one word could capture the 2025 housing and mortgage market, it would be change – a year marked by major shifts across the housing and mortgage landscape.

Here’s an industry recap for November 2025:

Prices, Inventory & Sales Activity

- – Nationwide, home prices remain elevated compared with a year ago, but price appreciation has slowed, and some markets show signs of moderation under rising supply pressure.

- – Single family inventory remains elevated as listings have surpassed 1 million active homes for sale. Listings are staying on the market longer than a year ago with an average of 63 days on the market as compared to 46 days in 2024 as reported by REALTOR.com.

- – As a result, the market is appearing more balanced than during the red-hot post-pandemic years.

Mortgage Rates & Borrowing Conditions

- – According to Freddie Mac for the week ending November 26, the average 30-year fixed-rate mortgage was ~6.23%.

- – Shorter-term and adjustable-rate mortgages reflect similar modest declines: 15-year fixed rates are generally in the 5.5%–5.6% range.

- – Overall, mortgage rates are roughly 50–60 basis points lower than they were around the same time last year, making borrowing somewhat more attractive than in late 2024.

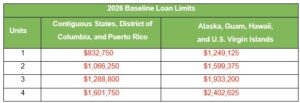

New Conforming Loan Limits

The Federal Housing Finance Agency (FHFA) announced in November the new 2026 conforming loan limits for mortgages eligible for purchase by Fannie Mae and Freddie Mac. The limit will increase from $806,500 in 2025 to $832,750 in 2026—an uptick of $26,250. Under the Housing and Economic Recovery Act (HERA), FHFA adjusts these limits annually to reflect changes in the national average home price.

What’s Driving the Market and What’s Holding It Back

Drivers of the current market

- – Existing mortgage rates are still weighing on affordability, discouraging many potential buyers – particularly first-time buyers. Many continue to hope for rate decreases to pandemic/post-pandemic levels. Just remember that some define hope as that thing you cling to until reality shows up.

- – The fact that many existing homeowners have locked-in low mortgage rates reduces seller motivation to move; this lowers turnover and keeps housing supply artificially constrained. About 52% of outstanding mortgages in the U.S. had rates below 4.00%.

- – On the other hand, recent rate declines and larger housing inventory are giving some buyers more choices which may partly explain a modest rebound in homes sales activity going into the 4th quarter of 2025.

- – Incentives to Refinance – As rates have dropped, a growing number of borrowers, especially those who originated loans during 2023–2024, are now “rate‑able,” meaning they could save money by refinancing.

Headwinds and challenges

- – Home prices remain elevated relative to historical norms. Zillow reports U.S. home values have increased over 45% since early 2020. This appreciation includes a mix of factors: demand surge during/after the pandemic, tight supply, rising construction costs, etc.

- – According to the National Association of Home Builders confidence of their members is weak, and new construction is subdued. That limits the supply of new homes – meaning alleviating affordability may be a slow, drawn-out process.

- – Regulatory and government overreach remain a constant challenge to the real estate and mortgage finance industries. Rumors of the dissolution of the – Consumer Financial Protection Bureau (CFPB) continue as mortgage lenders ask what a world without the CFBP would look like. Regulation is not always a bad thing, but most agree some regulations on the federal, state, and local levels can go too far. A humorous case in point – Did you know it is illegal for you to pump your own gas in the state of NJ? Since 1949 under the Retail Gasoline Dispensing Safety Act, it is illegal for a consumer to “fill er up”.

- – Hidden Homeownership Expenses Raise to Record Highs– While interest rates and elevated home prices continue to challenge homeowners, rising costs for insurance and property taxes are becoming more impactful in the affordability equation. Since 2020, nationwide home insurance premiums have jumped 48%, pushing the average policy above $2,200.

What to Watch for in the Months Ahead

- – More analysts and industry experts – including Redfin – are expecting a gradual “housing reset” in 2026. However, affordability pressures will continue as high prices relative to incomes continue to constrain buyers.

- – Interest rates: Mortgage rates remain the single biggest factor influencing buyer demand. Even small shifts can affect affordability and refinancing activity.

- – Federal Reserve & monetary policy: Fed actions on interest rates, inflation targets, and bond purchases will continue to ripple through mortgage pricing.

- – The behavior of existing homeowners — whether they stay put or decide to sell — will have outsized influence on inventory and market dynamics.

Bottom Line

November 2025 shows a U.S. housing market in slow transition: price growth is modest but still positive, housing supply is rising, and mortgage rates have eased enough to rekindle some buyer interest. However, persistent affordability challenges, cautious builders, and deeply rooted, “low-rate mortgage lock-in” means any full rebound will likely be gradual rather than a quick turnaround.

We now know December has not always been the 12th month on the calendar. Here’s another December fact – It brings the shortest days and longest and darkest nights of the year in the Northern Hemisphere with the arrival of the winter solstice. While this month may be dark outside, the Canvas Mortgage Team is committed to closing out 2025 on a very bright note with many families still to serve as we close their mortgage loans before year-end. At the same time, we look forward to enjoying to a bright holiday season with family and friends celebrating, relaxing, and making memories. From all of us at Canvas Mortgage, we wish our entire Merchants & Marine family of brands a very Merry Christmas and a New Year filled with joy and blessings.